For decades, traditional investment avenues – equities, fixed deposits, mutual funds – have served as the backbone of Indian portfolios. But a new wealth frontier is rising quietly yet powerfully across India’s financial landscape: Alternative Investment Funds (AIFs).

Over the last few years, AIFs have moved from being an ultra-niche asset class to a mainstream allocation for India’s wealthy, family offices, UHNI investors, and sophisticated professionals. And the reason is simple: AIFs provide access to opportunities that traditional investments cannot offer.

From pre-IPO investments and venture capital to private credit, distressed assets, startup funding, and SME growth capital, AIFs are now shaping India’s next phase of wealth creation.

1. India’s Explosive AIF Growth: A Market Too Big to Ignore

The AIF industry is expanding faster than any other financial segment in India.

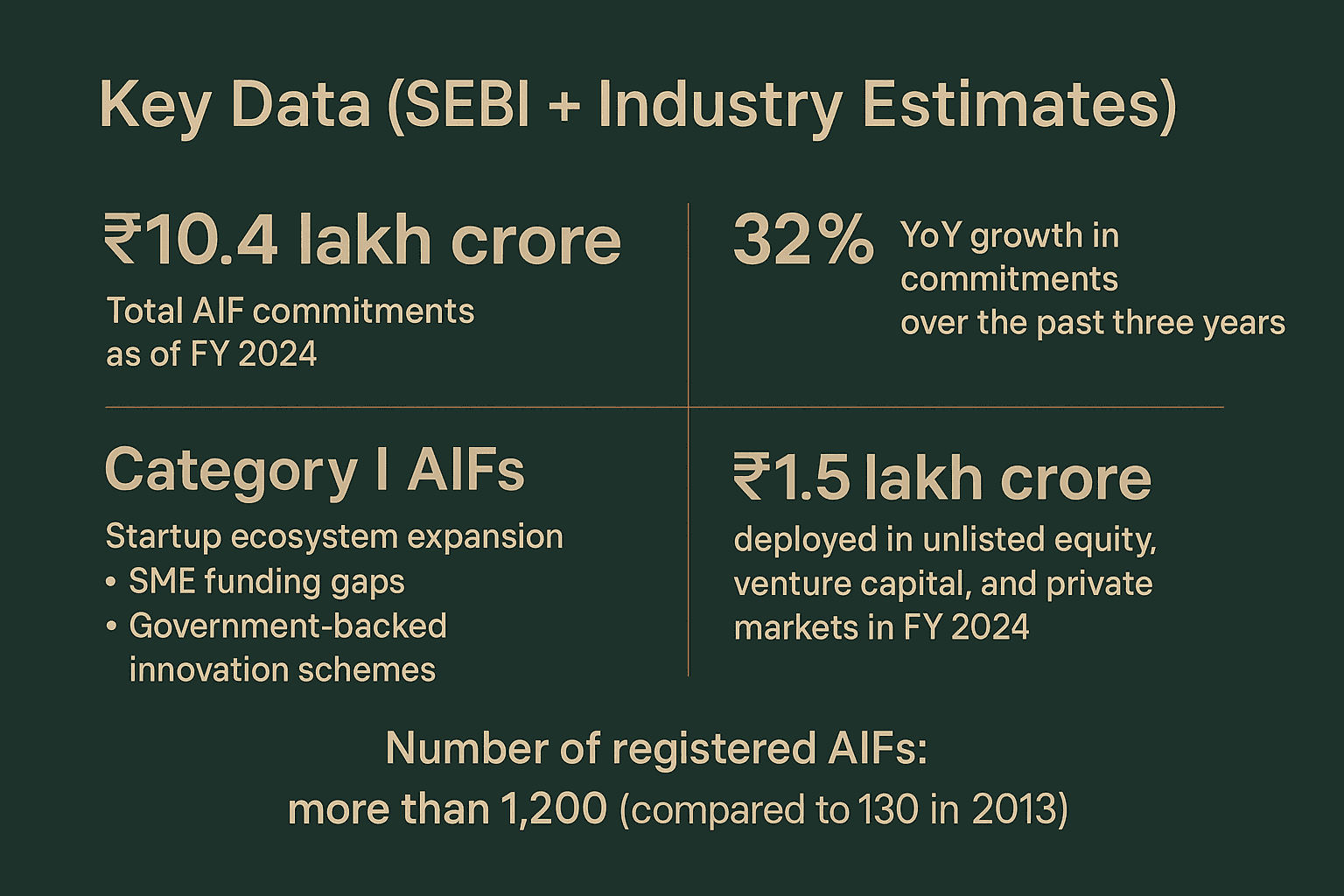

Key Data (SEBI + industry estimates):

In simple words -AIFs are becoming a core pillar of modern Indian wealth portfolios.

2. Why AIFs Are Unlocking a New Wealth Frontier

Traditional investments remain important, but they have limitations:

Public markets are crowded

Debt yields have compressed

Mutual funds have become highly benchmarked

Excess liquidity reduces alpha

AIF solve these pain points by providing access to private, high-growth, less-correlated opportunities.

AIF Advantages Driving Massive Demand:

A. Access to Private Markets

You get exposure to:

High-growth startups

Pre-IPO companies

SME expansion capital

Private equity deals not available on exchanges

B. Higher Alpha Potential

Private assets historically outperform public markets when chosen carefully.

C. Diversification Beyond Equities & Debt

Low correlation protects against market volatility.

D. Expert, Research-Driven Management

AIFs are run by fund managers who specialise in niche categories like:

Venture capital

Distressed credit

Real assets

Manufacturing growth

Clean energy

E. structured Risk Management

Many AIFs follow:

Deal-level due diligence

Precision monitoring

Risk-based underwriting

This professional approach is why HNIs trust AIFs for long-term wealth creation.

3. AIFs and India’s Emerging Market Opportunities

India is entering a golden decade, driven by four structural tailwinds:

A. Demographics: A Young, Earning India

By 2030, India will add 140 million new consumers to the middle-income bracket.

Consumption-led sectors and digital businesses will explode.

B. Startup Ecosystem: Third-Largest in the World

More than 95,000 startups

Over 110 unicorns

Strong government support: Startup India, SIDBI Fund of Funds

Category I AIFs are the gateway to capturing this early-stage wealth creation.

c. SME Growth: The Real India Story

India has 6.3 crore SMEs but only a tiny fraction access equity financing.

Category I SME-focused AIFs are solving this gap -and generating attractive returns.

4. How Investors Are Allocating to AIFs

HNIs Allocation Trends (FY 2024 Reports):

Average wealthy investor allocation to AIFs: 12 percent to 18 percent

Family offices allocation: 20 percent to 35 percent

Pre-IPO + VC + Private credit are the fastest-growing themes

Why?

Because sophisticated investors are chasing:

Higher alpha

Early access

Non-market-linked wealth creation

5. Category I AIFs: The Real Engine of India’s Growth

Category I AIFs (Startup, SME, Venture Capital) are directly aligned with India’s future.

They support:

Early-stage innovation

Manufacturing expansion

MSME formalisation

Job creation

Technology enablement

And they benefit from:

Tax & regulatory support

Government co-funding in certain sectors

Highest economic multiplier effect

For investors, Category I AIFs offer:

Long-term compounding

Access to sunrise sectors

Significant diversification

Exposure to companies before the masses can invest

This is why Category I AIFs are expected to grow at 28 to 35 percent annually till 2030.

6. The New Age of Private Market Investing: What It Means for Investors

The wealth playbook is changing.

Earlier, the Indian investor journey looked like this:

FD → Equity → Mutual Fund → Real Estate

Today, the evolved investor journey is:

Equity → PMS → AIF → Pre-IPO → Direct Private Investments

This shift is driven by:

More financial awareness

Desire for higher-growth assets

Access to institutional investment vehicles

India’s strong private market story

AIFs sit at the center of this new investment ecosystem.

7. Should AIFs Be Part of a Modern Indian Portfolio?

Yes - and here’s why:

They offer exposure to growth :

Non-linear returns

Long-term compounding

Access to exclusive private-market deals

Portfolio balance during volatility

For sophisticated investors, AIFs are no longer optional -they are strategic.

Conclusion: AIFs Are Defining the Next Chapter of Indian Wealth

India’s investment landscape is evolving faster than ever. And as traditional assets mature, the next wave of wealth creation is happening inside the private markets -powered by AIFs, venture capital, pre-IPO deals, and SME growth capital.

AIFs don’t just offer returns.

They offer access, diversification, and participation in India’s growth story long before it becomes visible in public markets.

As India heads toward a multi-decade economic expansion, AIFs will remain one of the most powerful vehicles for building generational wealth.

Ekamya Capital stands positioned at the intersection of these opportunities -helping investors access new wealth frontiers with discipline, research, and institutional-grade advisory.

FAQ:

1. What is an Alternative Investment Fund (AIF)?

An AIF is a pooled investment vehicle regulated by SEBI that invests in alternative assets such as private equity, venture capital, startups, SME debt, and pre-IPO companies.

2. Why are AIFs becoming popular in India?

AIFs offer access to high-growth private markets, better diversification, and potential for higher alpha compared to traditional equity or mutual funds.

3. Are AIFs regulated by SEBI?

Yes, AIFs operate under strict SEBI guidelines covering fund structure, reporting, compliance, and investor protection norms.

4. What are the different categories of AIFs?

SEBI classifies AIFs into:

Category I: Startup, SME, VC, social impact funds

Category II: Private equity, debt, distressed assets

Category III: Hedge-style long-short strategies

5. Who should invest in AIFs?

AIFs are ideal for HNIs, UHNIs, family offices, and sophisticated investors looking for long-term, high-growth opportunities in private markets.

6. How do AIFs unlock new wealth frontiers?

They give investors early access to startups, pre-IPO companies, private credit, and niche sectors that are not available in public markets.

7. What is the minimum investment in an AIF?

SEBI requires a minimum investment of ₹1 crore per investor, except for employees or directors of the fund where lower limits may apply.

8. How are AIFs taxed in India?

Category I and II AIFs are pass-through for most income, while Category III is taxed at the fund level. Taxation varies based on the asset class and income type.

9. What is the risk level in AIF investments?

AIFs carry higher risk than traditional investments because they invest in private, less-liquid, and high-growth assets. However, they offer higher return potential.

10. Which AIF category is the best to invest in?

SEBI does not publicly disclose individual AIF return data, insights. so, there is no “best” category overall, only the best category for your goals, risk appetite, and investment horizon. but as per historical performance trends of AIFs in India, Category I AIFs (Startup, VC, SME) gives highest Returns along with Highest Risk