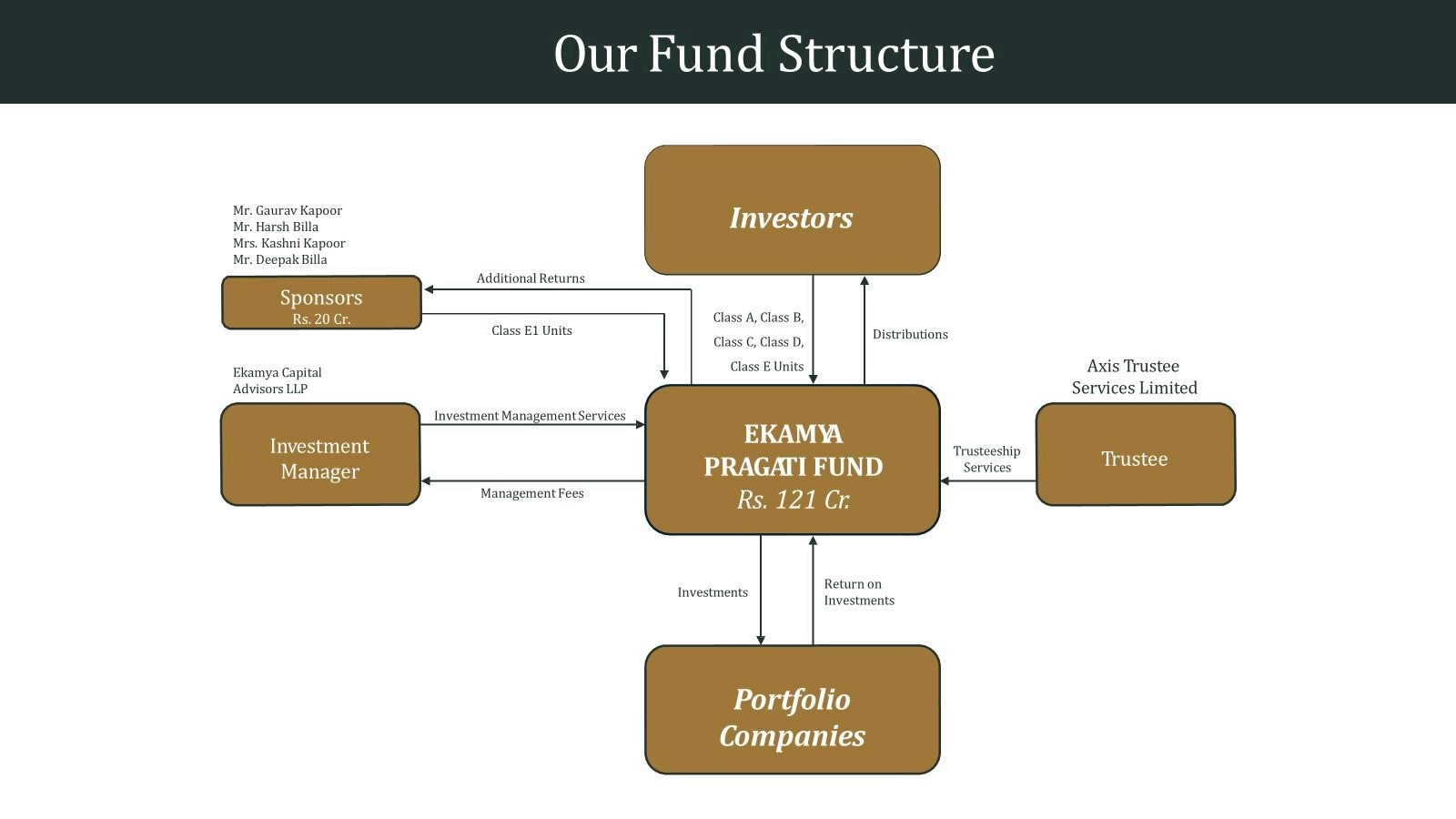

Alternative Investment Funds (AIFs) have quickly moved from being a niche product to a mainstream allocation for sophisticated Indian investors. As public markets become crowded and traditional products like fixed deposits and mutual funds deliver predictable returns, HNIs and family offices are actively exploring AIFs for better diversification, higher alpha, and access to private-market opportunities.

But the big question most investors ask is simple:

How exactly can I invest in an AIF in India? What is the minimum capital required? What is the process?

This guide covers everything you need to know — clearly, practically, and based on SEBI regulations.

What Is an AIF (Alternative Investment Fund)?

An AIF is a privately pooled investment vehicle registered with SEBI that invests in non-traditional asset classes such as:

Venture capital

Private equity

SME growth capital

Pre-IPO shares

Private credit

Distressed assets

Long–short hedge strategies

AIFs are typically used by HNIs, UHNIs, institutions, and professionals who want exposure beyond public markets.

Minimum Investment Required to Invest in an AIF

SEBI has defined clear minimum-ticket size rules:

Minimum investment: ₹1 crore per investor

This applies across all three AIF categories.

Exceptions:

Fund employees or directors: ₹25 lakh minimum

Accredited investors (as per SEBI): lower limits may apply depending on fund structure

Why such a high minimum?

AIFs involve higher risk

Longer lock-ins

Private-market volatility

Need sophisticated investor understanding

This ensures that only informed and financially sound investors participate.

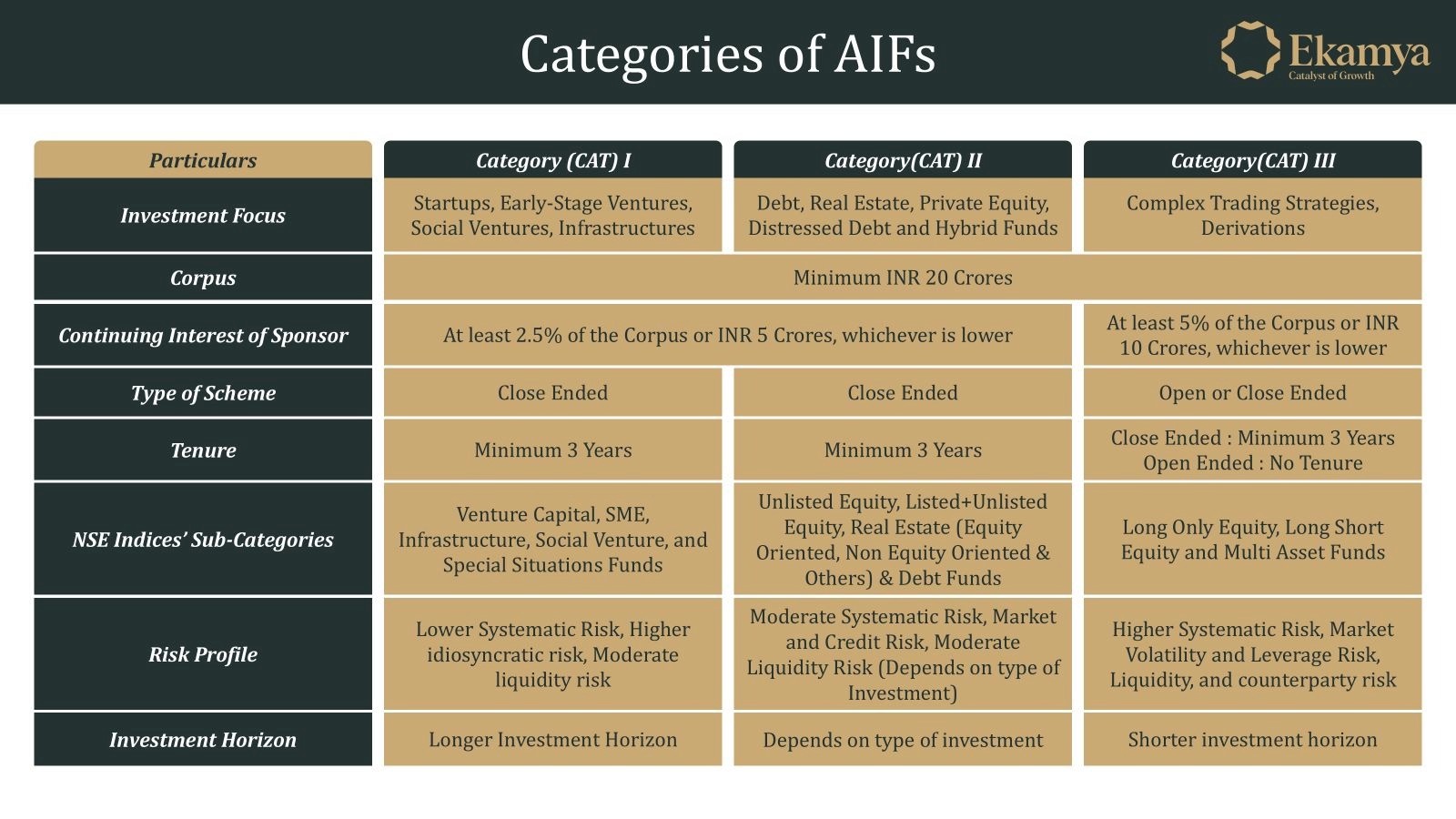

Types of AIFs You Can Invest In

SEBI classifies AIFs into three categories:

Category I AIFs

Includes startup funds, SME funds, early-stage VC, and social impact funds.

Best for: Investors seeking high-growth, long-term private-market exposure.

Category II AIFs

Includes private equity, private credit, real estate, distressed asset funds.

Best for: Balanced growth + stability, predictable income (in private credit).

Category III AIFs

Includes long–short equity funds and hedge-fund style strategies.

Best for: Market-savvy investors aiming for hedged returns.

Step-by-Step Process to Invest in an AIF in India

The AIF investment process is professional and structured. Here is the exact sequence:

Step 1: Choose the Right Category and Strategy

Start by understanding:

Your risk appetite

Lock-in tolerance

Growth expectations

Tax implications

Sector preferences (startups, PE, credit, pre-IPO, etc.)

Tip: Category II (PE + Credit) offers the most balanced risk-return profile for most HNIs.

Step 2: Assess Fund Performance and Manager Expertise

Before investing, evaluate:

Track record of fund manager

Past IRRs

Portfolio diversification

Experience across market cycles

Risk management policies

Strong manager capability is the biggest success factor in AIFs.

Step 3: Complete KYC and Eligibility Checks

You must complete:

PAN

Aadhaar

Address proof

Bank proof

Income or net-worth eligibility

FATCA declaration

Accredited investors may require additional documentation.

Step 4: Review the Fund Documents

Essential documents include:

Private Placement Memorandum (PPM)

Contribution Agreement (CA)

Subscription Agreement

Risk disclosure document

The PPM outlines strategy, risks, fees, lock-in, exit policy, valuation method, and governance structure.

Step 5: Commit Capital and Complete Subscription

After agreement review:

Sign the Subscription Agreement

Transfer the minimum commitment (₹1 crore)

Complete onboarding and advisor documentation

Some funds use capital call (drawdown) structures where money is taken in tranches.

Step 6: Fund Deployment and Reporting

Once invested:

Fund manager deploys capital into deals

You receive quarterly or semi-annual reports

Valuation updates shared periodically

Tax statements provided annually

AIF investors must be comfortable with longer investment horizons (4–8 years depending on category).

Fees and Charges You Should Know

AIFs typically follow an institutional fee model:

Management Fees:

1%–2.5% annually depending on category

Performance Fees (Carry):

10%–20% on profits above hurdle rate

Setup / administrative charges:

Varies by fund

Understanding the fee structure helps in comparing fund performance fairly.

Risks : Investing n AIF

AIFs offer high-growth potential but come with risks:

Illiquidity (long lock-ins)

Higher volatility in private markets

Dependence on manager skill

Market cycle impact

Regulatory and taxation changes

Invest only with fund houses that maintain strong due diligence, governance, and transparency.

Taxation Rules for AIF Investments

Tax treatment differs by category:

Category I & II AIFs

Pass-through structure

Capital gains taxed in investor’s hands

Interest or dividend income taxed as per investor slab

Category III AIFs

Taxed at the fund level

Business income taxed at 42.744% (surcharge + cess included)

Capital gains taxed at normal rates

Always consult a tax specialist to structure your investments effectively.

Who Should/ Can Invest in AIFs?

AIFs are ideal for:

HNIs and UHNIs

Family offices

NRIs (subject to FEMA)

Professionals with surplus capital

Investors looking for non-market linked returns

Investors seeking pre-IPO, PE, and private market exposure

If you have a long-term horizon and a higher risk appetite, AIFs can play a major role in wealth creation.

Conclusion: AIFs Offer Access to India’s Most Powerful Emerging Opportunities

AIFs have become a core pillar of modern Indian wealth management because they unlock:

Early access to high-growth companies

Better diversification

Potential for superior returns

Exposure to private markets

A hedge against public-market saturation

As India continues its economic expansion, sophisticated investors are increasingly allocating to AIFs to participate in the country’s next decade of wealth creation.

Ekamya Capital helps investors access carefully curated AIF opportunities with transparency, research-driven selection, and disciplined portfolio strategy.