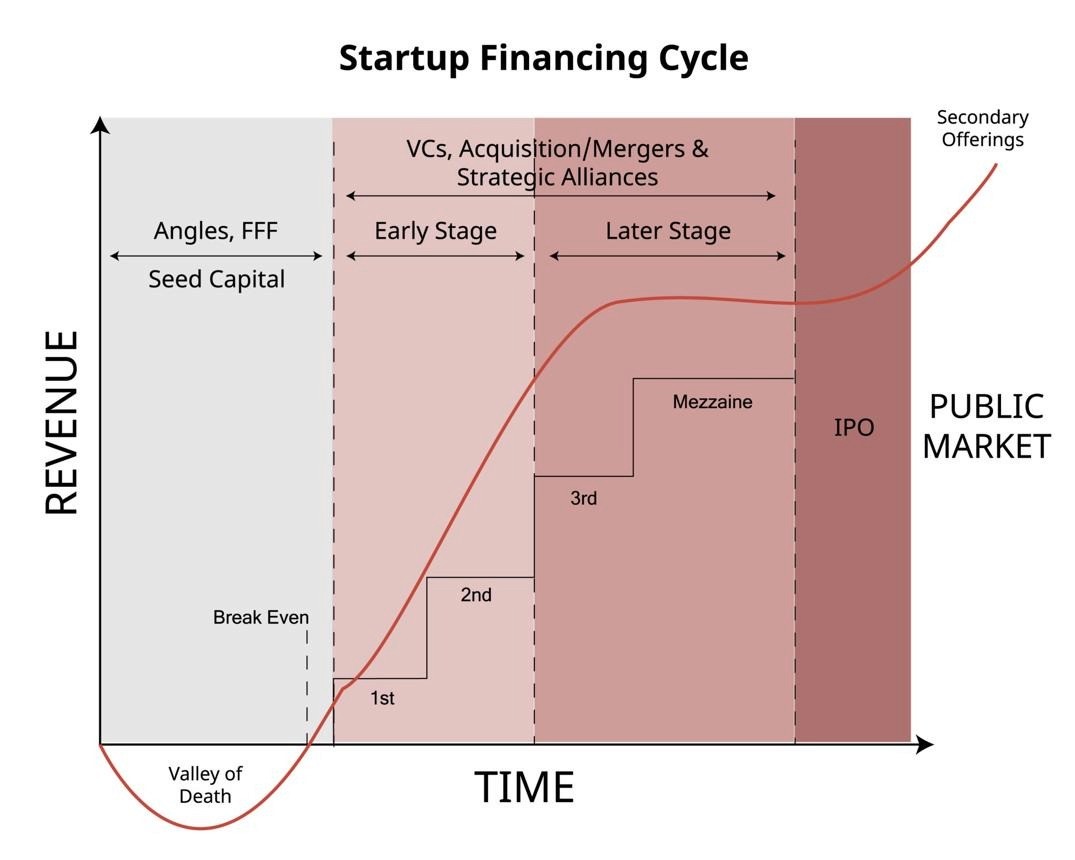

Most founders walk into investor meetings believing the same story: build a great product, raise Pre-Seed funding, then Seed, Series A, Series B, Series C, and eventually go public. In this version of reality, funding is a straight staircase where hard work and growth automatically attract capital. but the reality is very different. India had over 223,000 DPIIT- recognized startups as of 31 March 2026, with more than 55,000 added in FY 2025-26 alone. Yet only an estimated 1,200-3,500 startups have reached Series A or beyond, representing roughly 0.5-1.5% of the ecosystem. Put differently, a startup's chances of reaching Series A are often lower than even IITs and IIMs, where selection rates typically range between 1% and 2%. The number of startups that progress to Series C is even smaller can be counted in the hundreds, while those that successfully journey from a bootstrapped or angel-funded idea to an IPO remain exceptionally rare.

This is because funding stages are not a graduation system. They are risk-reduction checkpoints. Every round of funding reflects an investor's belief that a specific risk has been been reduced. Pre-Seed is a bet on the founder, Seed on the problem and early market signals, Series A on product-market fit, Series B on the business model, Series C on market leadership, and Pre-IPO on predictability and governance.

When you understand funding as risk reduction rather than reward for effort, the entire game changes - how you prepare, what you build, and how you communicate with investors. This blog will walk you through every stage of that journey, from Pre-Seed to IPO, with real data from the Indian market covering FY 2021-22 to FY 2025-26. More importantly, it will explain exactly what sophisticated VC investors are evaluating at each checkpoint - and where founders consistently get it wrong.

The VC Funding Lifecycle

Before going stage by stage, it helps to understand the underlying logic of how venture capital works as a system.

Venture capital is, at its core, a power law business. A fund manager raises capital from Limited Partners - family offices, HNIs, institutions, pension funds - with a promise of outsized returns. Typical VC fund life is 5 to 10 years. In that period, the fund must deploy capital, wait for startups to grow, and return multiples to investors. The math works only if 1 or 2 companies in a portfolio of 20 return 20x or more. The rest can fail, break even, or return modest gains - and the fund still works.

This is why VCs behave the way they do. They are not simply funding good businesses. They are hunting for the rare company that can return the entire fund - what the industry calls a "fund returner." Every investment decision is filtered through this lens, not through the lens of whether a business is solid, well-managed, or even profitable.

For Indian founders, this creates a specific dynamic. A VC investing from a $50 million fund needs at least one company to return $100 million. That company needs to reach a valuation of several hundred million dollars or more. So from the moment a VC sits across from you, they are not just asking whether your business is good. They are asking whether your business can be that company - the one that makes the entire fund.

Understanding this changes how you pitch, how you size your market, and how you frame your ambition. The stages that follow are not just about how much money changes hands - they are about what risk the capital is being deployed against, and whether the founder can credibly prove that risk is on its way out.

3. Stage-by-Stage Breakdown

3.1 Pre-Seed Stage

What is Pre-Seed stage funding?

The Pre-Seed stage is the earliest formalised capital a startup raises. In most cases, the company exists more as an idea, a thesis, or a very early prototype than a functioning business. There may be no revenue, no validated customer base, and sometimes no complete founding team. What exists is a conviction - in a problem, in a market gap, and in the people proposing to solve it.

In the Indian context, Pre-Seed funding typically comes from friends and family, individual angel investors, angel networks such as Indian Angel Network or LetsVenture, or early-stage micro-VCs that write small cheques. The amounts are modest - anywhere from $30,000 to $350,000 (roughly ₹25 lakh to ₹3 crore in FY2025-26 terms).

What investors evaluate?

At Pre-Seed, the product barely exists. So the investor is almost entirely evaluating the founder. This means a few specific things:

Founder-market fit is the primary signal. Does this person have a genuine, deep relationship with the problem they are trying to solve? Not surface familiarity - real lived experience, domain expertise, or years spent inside the industry where the problem lives. A founder who has spent a decade in cold chain logistics pitching a logistics-tech solution is fundamentally different from someone who read about the sector and decided to build in it.

Problem clarity is the second signal. Can the founder articulate, without jargon or slide dependency, exactly what breaks in the current system and for whom? The best Pre-Seed founders can explain the pain in one precise paragraph. When a founder needs five slides to define the problem, it usually signals they have not yet thought through it deeply enough.

Early signals - not traction - matter at this stage. A waiting list of 200 potential users, a letter of intent from a pilot customer, 10 user interviews that reveal a specific, recurring pain point - these carry far more weight than polished pitch decks. The investor is looking for proof that the founder is not building in a vacuum.

The reality

Pre-Seed is where most startup journeys begin and end. Failure rates here are difficult to track precisely because many companies fold before they even raise a formal round - they simply run out of personal savings or family support. Of those that do raise Pre-Seed capital, industry estimates suggest that 70 to 80% never progress to a Seed round. The reasons vary - poor timing, wrong market, founder conflict, inability to find product-market fit - but the common thread is that the gap between "promising idea" and "fundable business" is far wider than most founders expect.

3.2 Seed Stage

What it is Seed Stage Funding?

Seed is where the hypothesis gets its first real test. The company now has some version of a product - it may be rough, it may be changing rapidly, but there is something a user can interact with. The Seed stage is about finding out whether the problem the founder identified is real, whether the proposed solution resonates, and whether there is a sustainable path to building a business around it.

Seed funding in India typically ranges from $500,000 to $2.2 million (roughly ₹4-19 crore in FY2025-26.) Investors at this stage include angel networks, early-stage VC funds such as India Angel Network (IAN), Titan Capital, 100X.VC, FirstCheque, Ekamya Capital, Venture Catalysts, Better Capital and others as well as family offices that have an appetite for early-stage risk.

What investors evaluate

The Seed-stage investor is looking for early evidence that the market wants what the founder is building. This does not require polished revenue numbers, but it does require signal:

Early user engagement that suggests genuine demand, not just curiosity. Retention curves, repeat usage, and unsolicited referrals matter more than download counts. How much does the first user cohort actually use the product after the first week?

Problem validation from paying or highly engaged customers. Even if the product is free, is there a segment of users who would pay if asked? Are there early adopters who are pulling the product forward - asking for features, referring friends, complaining when it is down?

Founder-team completeness is also assessed more critically at Seed. The team needs to be capable of building the product and finding customers and managing early operations. A solo technical founder with no go-to-market thinking is a yellow flag. A founding team with complementary skills - product, business, domain - is a green one.

The shift that happens here

Seed is also where the first conversation about unit economics begins - not in precise numbers, because those numbers do not exist yet - but in conceptual clarity. Does the founder understand how the business will eventually make more from a customer than it costs to acquire and serve them? Can they articulate the customer acquisition hypothesis, even if it is unproven?

Seed-stage failure is common and often brutal. Many companies raise Seed capital, spend 18 months iterating, and are unable to find product-market fit before the money runs out. The ones that survive are typically those that either found a paying customer faster than expected, or discovered a pivot that better matched the original problem insight.

3.3 Pre-Series A / Series A - Where Storytelling Ends

What it is

The Pre-Series A is a bridge round that some startups raise when they have clear momentum but need 6 to 12 more months of runway to hit the metrics required for a Series A. It typically involves $2 million to $7 million (₹17 crore to ₹60 crore) in capital and is structured to get the company to a specific milestone - usually a revenue or retention target - rather than fund an extended phase of exploration.

Series A, on the other hand, is the first institutional round in the true sense. Raise sizes in India range from $6 million to $20 million (₹50 crore - ₹170 crore in FY2025-26.) This is the round where funds like Peak XV Partners (formerly Sequoia India), Accel, Lightspeed India, Ekamya Capital, Matrix Partners and others write their first meaningful cheques.

The critical shift

Series A is the most misunderstood round in the Indian startup ecosystem. Founders often believe that strong growth metrics - downloads, active users, gross merchandise value - will be sufficient to raise Series A. They are usually wrong.

What actually changes at Series A is that the conversation moves from qualitative to quantitative. The investor is no longer primarily evaluating the founder's conviction or the problem's significance. They are evaluating whether the business has found product-market fit - and the evidence must now be numerical, not narrative.

Specifically, investors focus on: revenue growth rate (month-on-month or year-on-year), net revenue retention (are customers staying and spending more?), customer acquisition cost (CAC) versus lifetime value (LTV), and gross margins (is the business structurally capable of being profitable at scale?).

The key insight is this: at Seed Stage, a compelling story can compensate for thin data. At Series A, the story must be supported by data. From this point forward, investors are running spreadsheet models, not just listening to pitches. Founders who have not built the financial discipline to track and report on unit economics in real time find themselves unable to raise Series A - regardless of how good their product is.

3.4 Series B - Proving the Machine Works

What it is

Series B is where startups prove that their growth is not just real but repeatable, scalable, and structurally sound. The company now has a functioning product, a clear customer acquisition process, early evidence of retention, and some form of unit economics that points toward eventual profitability.

Series B raise sizes in India range from $15 million to $55 million (₹125 crore to ₹475 crore in FY2025-26.) At this stage, larger funds - including international VCs with India presence - enter the picture. Tiger Global, Prosus, General Atlantic, and Avataar Venturesand others have all been active at the Series B level in India.

What investors evaluate

Series B investors are running a different analysis than Series A investors. They are not asking "does this business work?" - that question has already been answered. They are asking "does this business scale in a way that is economically rational?"

Unit economics must now be clear, not just conceptual. CAC payback period - how many months does it take to recover the cost of acquiring a customer - should ideally be under 18 months for a SaaS or B2B business. LTV-to-CAC ratios above 3:1 are the standard benchmark. Gross margins need to demonstrate that as the business grows, the financial structure improves rather than deteriorates.

Market expansion logic is another critical pillar. The investor wants to understand how the company moves from its current beachhead - the segment or geography where it first found traction - into adjacent markets. Is the core technology or distribution advantage transferable? Or is growth in new markets going to require essentially rebuilding the business from scratch?

Repeatability of the sales and growth process is the third lever. A startup that grew because of a handful of exceptional salespeople or because of a viral moment is a very different business from one that has built a systematic, teachable, process-driven growth engine.

3.5 Series C and Beyond - Playing for Dominance

What it is

By the time a startup reaches Series C and later growth-stage rounds, the character of the investors changes significantly. Large global VCs, private equity firms, and sovereign wealth funds begin to participate. In the Indian context, investors like GIC, Canada Pension Plan Investment Board (CPPIB), Temasek, and large domestic institutions such as HDFC Capital and Kotak Private Equity, and others have been active at this stage.

What investors evaluate

The evaluation framework here shifts from growth to quality of growth. Profitability visibility - not necessarily current profitability, but a credible path to EBITDA-positive operations - becomes a primary lens. In the post-2022 correction era, investors are particularly focused on whether the business can sustain itself without continuous capital infusions.

Market dominance is evaluated in terms of whether the company has built structural moats. Network effects, proprietary data advantages, regulatory relationships, brand loyalty, and switching costs are the kinds of defensibility that justify late-stage valuations. A company that is large but easily replicable is a poor late-stage investment, regardless of its current revenue.

Operational efficiency - revenue per employee, cost per transaction, infrastructure leverage - matters because at scale, these numbers determine whether the business is genuinely building value or simply converting investor capital into market share.

3.6 Pre-IPO

What is Pre -IPO Investment?

The Pre-IPO stage is qualitatively different from every earlier round. The in this stage company is no longer being funded to grow - it is being groomed to be a public company. This means the investment thesis shifts from growth potential to earnings predictability, governance quality, and public market readiness.

What investors evaluate

In the Pre-IPO stage(also called Late Stage), EBITDA trajectory and path to sustained profitability are the headline metrics. The investment banker community, which now plays an active role in preparing the company for public markets, requires at least 2 to 3 quarters of clean, improving financial results. Revenue predictability - not just revenue growth - is what the public market will eventually pay for.

Governance and institutional readiness are evaluated seriously. This means an independent board with experienced directors, audited financials prepared under Indian GAAP or IFRS, functioning audit and risk committees, and clean cap table structures. SEBI compliance readiness is checked in detail. Founders who have been sloppy about governance in earlier stages find this phase deeply painful.

Founder liquidity is also a consideration at this stage. Many Pre-IPO investors negotiate secondary share purchases, allowing early investors and founders to take some money off the table. This is a structural feature of the late stage that earlier-stage investors rarely offer.

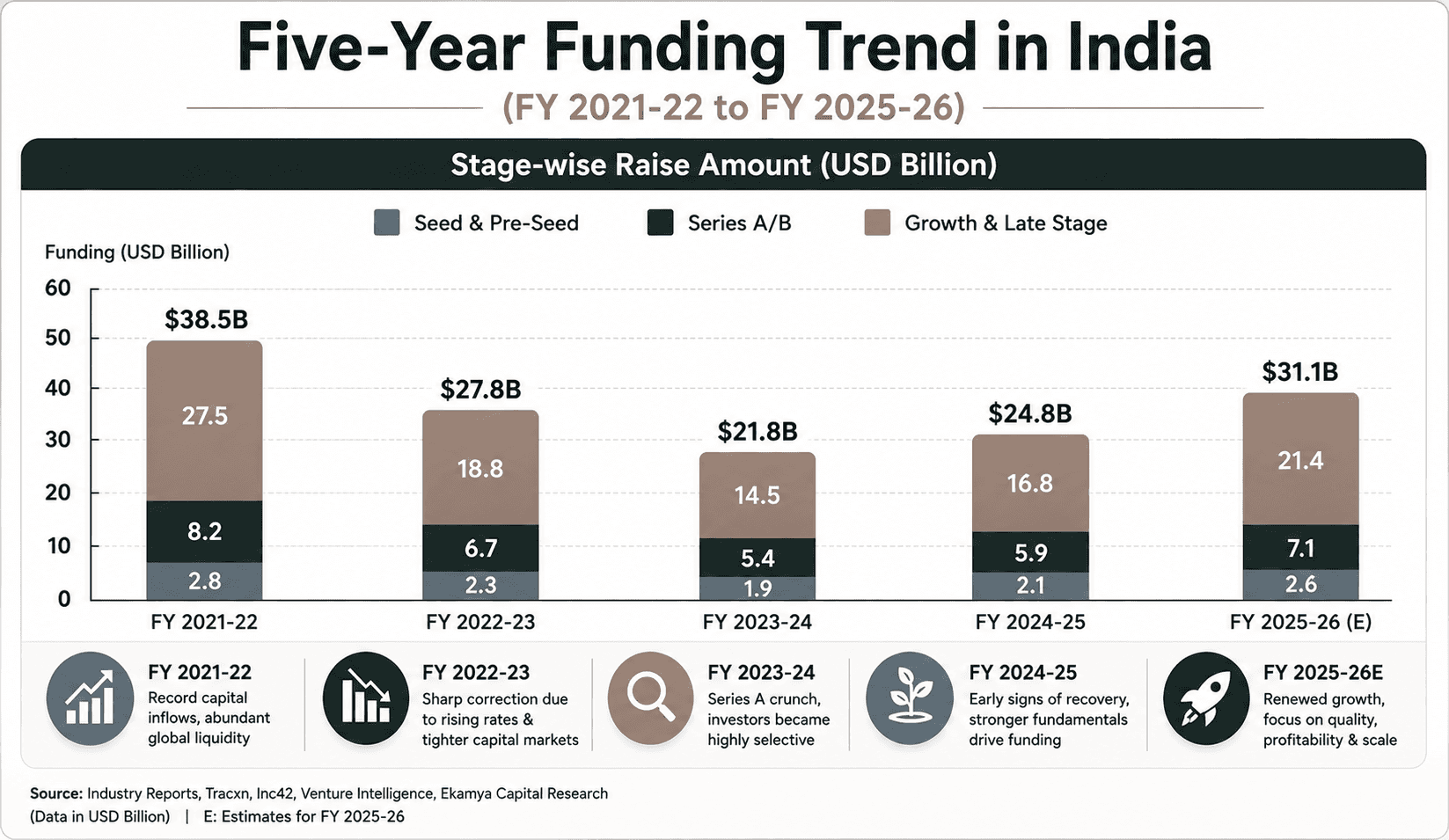

4. Five-Year Funding Trend in India (FY 2021-22 to FY 2025-26)

The five financial years from FY2021-22 to FY2025-26 represent one of the most volatile and instructive periods in Indian startup history. Understanding what happened - and why - is essential for any founder or investor operating in this market.

FY 2021-22: Record Capital Inflows ($38.5 Billion)

India witnessed one of its strongest funding years, with total startup funding reaching $38.5 billion. Growth and late-stage companies alone attracted $27.5 billion, supported by abundant global liquidity, low interest rates, and strong investor confidence.

FY 2022-23: Market Correction Begins ($27.8 Billion)

Total funding declined to $27.8 billion, a drop of nearly 28% YoY. Growth-stage funding fell from $27.5 billion to $18.8 billion, as investors became cautious amid rising interest rates and global economic uncertainty.

FY 2023-24: Series A Crunch & Investor Selectivity ($21.8 Billion)

Funding reached its lowest point at $21.8 billion. Series A/B funding dropped to $5.4 billion, while growth-stage investments declined further to $14.5 billion. Investors shifted focus toward profitability, governance, and capital efficiency.

FY 2024-25: Early Recovery Phase ($24.8 Billion)

Funding activity began recovering, with total capital raised increasing to $24.8 billion. Growth-stage funding improved to $16.8 billion, while Series A/B funding rose to $5.9 billion, reflecting improving market sentiment and stronger startup fundamentals.

FY 2025-26E: Return of Growth with Discipline ($31.1 Billion)

Total startup funding is estimated to reach $31.1 billion, representing a strong recovery from the downturn. Growth-stage funding is projected at $21.4 billion, while Series A/B funding could reach $7.1 billion. Unlike FY 2021-22, capital deployment is expected to be driven by profitability, governance, and sustainable growth rather than aggressive valuation expansion.

5. Investor Behavior - Who Invests at Each Stage

Understanding who invests at each stage is as important as understanding how much they invest. The type of investor shapes the terms, the support, the timeline, and the strategic value of the capital.

Stage | Angels / HNIs | Family Offices | Early-Stage VCs | Growth VCs / PE |

|---|---|---|---|---|

Pre-Seed | 70–90% | 5–15% | 5–10% | Rare |

Seed | 40–60% | 15–25% | 25–40% | Rare |

Pre-Series A | 10–20% | 20–30% | 50–65% | 5–10% |

Series A | 5–10% | 10–20% | 65–80% | 10–15% |

Series B | Rare | 5–10% | 40–55% | 40–55% |

Series C | None | 5–10% | 20–35% | 60–75% |

Late / Pre-IPO | None | 5–10% | 10–15% | 75–90% |

Key dynamics to understand:

Angels dominate the earliest stages because they have the highest risk tolerance and the most flexible decision-making process. An angel can decide to invest in a conversation. A VC fund has an investment committee, a due diligence process, legal documentation, and portfolio considerations. Angels also bring informal mentorship, introductions, and domain knowledge that formal funds often cannot provide at this stage.

Family offices - and India has a rapidly growing number of sophisticated family offices, particularly in Mumbai, Delhi NCR, and Bengaluru - are increasingly active at the Pre-Series A and Series A stages. They can write larger cheques than angels, move relatively quickly, and are less constrained by the fund return mathematics that govern VC decision-making. The Ekamya Capital approach, as a SEBI-registered AIF category-I fund, reflects exactly this shift: institutional discipline applied to early and growth-stage Indian businesses.

Venture capital funds dominate Series A through Series B. This is where the formal term sheet, board seat, and milestone-linked capital deployment structures become standard. VC investors bring portfolio network access, hiring support, and follow-on capital reserves - but they also introduce governance expectations and performance benchmarks that founders must be prepared to meet.

Private equity enters at Series C and beyond. PE investors apply a fundamentally different return calculus - they are less comfortable with open-ended growth narratives and more focused on operational cashflow, EBITDA multiples, and exit horizon clarity. Late-stage PE investment is where the company transitions from being valued on growth potential to being valued on earnings power.

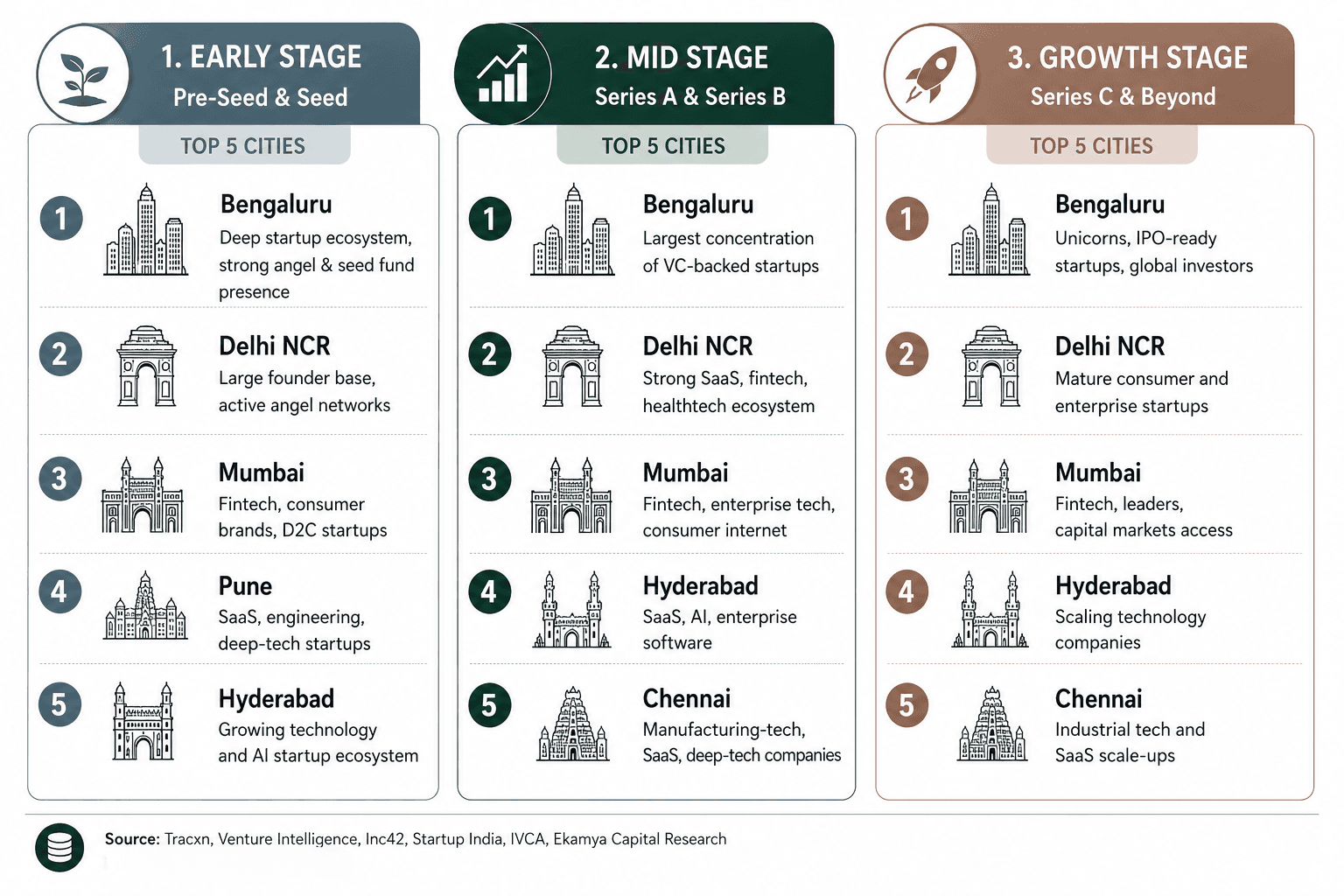

6. City-Wise Investment Patterns in India

Geography plays an important but often underappreciated role in startup funding in India. Capital does not flow uniformly across the country - it concentrates in specific cities at specific stages, driven by ecosystem density, talent availability, and proximity to institutional capital.

Early Stage - Pre-Seed and Seed

The early-stage ecosystem is dominated by Bengaluru, which accounts for approximately 35 to 40% of all early-stage deals in India. The presence of a deep engineering talent pool, a mature angel investor community, and a culture of startup formation dating back to the Infosys-Wipro era makes Bengaluru the natural home for first-time founders.

Delhi NCR - particularly Gurgaon and Noida - is the second most active early-stage geography, accounting for 20 to 25% of early-stage activity. The NCR ecosystem has developed rapidly over the past decade, with fintech, edtech, B2B SaaS, and consumer internet startups finding strong early support from Delhi-based angels and early-stage funds. As one of the top VC firms in Gurgaon, Ekamya Capital operates from Sector 58, Gurugram - at the heart of this ecosystem.

Mumbai contributes 15 to 20% of early-stage deals, with particular strength in fintech, media, and consumer brand startups. Pune, Hyderabad, and Chennai collectively account for the remaining 15 to 25%, with Hyderabad showing accelerating growth particularly in deep-tech, healthtech, and government-linked technology businesses.

Mid Stage - Series A and Series B

At Series A and B, the geographic concentration intensifies. Bengaluru maintains its dominance at 45 to 50% of deals. Mumbai becomes more prominent - particularly for fintech, financial services, and consumer companies - rising to 25 to 30% of activity. Delhi NCR holds at 15 to 20%.

The key dynamic at mid-stage is that companies must often demonstrate that their model works beyond their home city. Bengaluru-based B2B companies are expected to show enterprise customers in Mumbai, Delhi, and Hyderabad. Consumer companies need to show national cohorts, not just metro concentration.

Growth Stage - Series C and Beyond

Late-stage capital follows financial infrastructure. Mumbai, as India's financial capital, leads late-stage deal activity due to its proximity to institutional investors, investment banks, and capital market infrastructure. Bengaluru remains strong, particularly for technology companies.

At this stage, the city where the company operates matters less than the sophistication of its investor base and the depth of its governance and reporting infrastructure. Companies raising Series C and Pre-IPO rounds are often simultaneously working with investment bankers, audit firms, and legal counsel spread across multiple cities.

Conclusion

The journey from Pre-Seed to IPO is rarely linear, and very few startups successfully navigate every stage. While funding rounds are often viewed as milestones, experienced investors see them as proof points that specific risks have been reduced. Founders who understand this shift in perspective position themselves far more effectively for long-term success. India's startup ecosystem continues to mature, with capital increasingly flowing toward businesses that demonstrate strong fundamentals, disciplined execution, clear governance, and sustainable growth. Whether you are raising your first angel cheque or preparing for a Pre-IPO round, understanding what investors evaluate at each stage can significantly improve your fundraising outcomes. Ultimately, successful fundraising is not about telling a compelling story alone, it is about building a business that consistently earns investor confidence at every stage of its growth journey.

If you found this useful, explore more from Ekamya Capital:

Disclaimer:

The information in this article is based on publicly available sources, industry reports, proprietary databases, and Ekamya Capital research. It is provided for informational purposes only and should not be considered investment, financial, or legal advice. Readers should independently verify all information before making any investment or business decisions.